Key Points

- A carbon tax is a cost-effective way to correct for environmental costs imposed by the production of the energy sector.

- A carbon tax can produce substantial revenue that can be used to lower other taxes, reduce the deficit, or redistribute income.

- A carbon tax would reduce carbon dioxide emissions, but by how much is uncertain.

Environmental Taxation

Editor’s Note: This article is part of a series of tax-related articles sponsored by the Penn Wharton Budget Model and the Robert D. Burch Center at Berkeley. All of the articles in this series are forthcoming in a book by Oxford University Press, co-edited by Alan Auerbach and Kent Smetters.

Environmental Taxation examines environmental tax-policy reforms, in particular a carbon tax. Robert C. Williams (2016) finds that a carbon tax is a cost-effective way to reduce greenhouse gas emissions. When implementing an environmental tax, however, it is important to consider the cost of implementation, effects on the economy, and who bears the burden of the tax.

Carbon emissions are an example of a market failure. When carbon dioxide (CO2) is released into the environment during the production of or use of a commodity, the CO2 harms someone other than the buyer or the seller, and neither the buyer nor the seller pays for that harm. Market failures can lead to an inefficient allocation of capital. For instance, in the case of CO2, society may make more products that release CO2 than would be efficient if buyers and sellers of CO2-generating products bore the full cost. Theoretically, a market failure can impede economic growth.

Economists often call an environmental tax to correct a market failure a Pigouvian tax. One problem with implementing an environmental tax is that it is difficult to calculate the harm to others caused by the market failure. In addition, an efficient environmental tax would allow for market flexibility across emitters and different methods of reducing emissions. A carbon tax will reduce CO2 emissions, but by how much is uncertain.

Williams (2016) finds that a tax on CO2 emissions is easy to implement. CO2 emissions are easy to monitor, since 94 percent of emissions are from the combustion of fossil fuels. In addition, CO2 emissions depend on only the carbon content of fuel, so taxing a few thousand fossil fuel firms can cover the vast majority (80 percent) of U.S. CO2 emissions. Williams notes that other greenhouses gases like Hydrochloroflourocarbons could also be added easily to the environmental tax base, while other gases may be harder to track.

The worldwide cost of CO2 emissions is estimated to be $43 per ton of CO2 emissions. However, the U.S. cost of CO2 emissions is estimated to be only $4 to $5 per ton of CO2 emissions. Williams (2016) finds that it is most efficient for the full carbon-tax rate to be implemented immediately rather than fazed in. Moreover, changes to the tax rate optimally follow changes to the cost of CO2 emissions.

A carbon tax is likely to have a negative impact on Gross Domestic Product (GDP) and be regressive. A carbon tax is regressive because energy is a larger portion of the budget for households with lower incomes. However, a carbon tax is less regressive than it first appears when the impact of a carbon tax on the prices of all goods is considered rather than only the impact on the price of energy.

The U.S. has low environmental taxes relative to other advanced countries both in terms of tax revenue and GDP. Figure 1 shows that the average environmental tax rate in other Organization for Economic Co-operation and Development (OECD) countries is 2.23 percent of GDP while in the U.S. it is only 0.9 percent of GDP.

Figure 1: Environmental Tax Revenue as a Share of GDP

Source: Metcalf (2009)

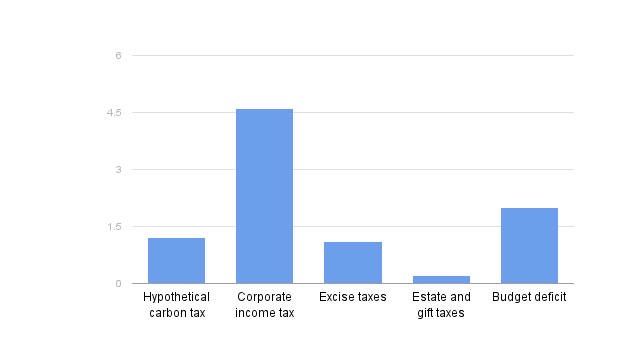

However, a carbon tax will also likely produce substantial revenue. The United States ran budget deficit of $439 billion in 2015, according to the Congressional Budget Office (CBO). When applying methods used by Joint Committee on Taxation (JCT) and CBO, Figure 2 shows that a carbon tax will produce a net revenue to the government of $1.7 to $1.2 trillion over the next 10 years. In comparison, the corporate income tax is estimated to generate $4.6 trillion in revenue in the next 10 years and the budget deficit is estimated to be $2 trillion over the same time period.

Figure 2: Estimated Revenue in Trillions of Dollars over Next 10 Years

Source: CBO (2015)

Note: The vertical axis is trillions of U.S. dollars. The revenue estimate from the hypothetical carbon tax is based on a tax of $25 per ton of carbon that rises at two percent per year in real terms and represents net revenue after accounting for the effects of the carbon tax on revenue from other taxes.

The extra tax revenue could be spent in several different ways, each with a different outcome. Figure 2 shows that a carbon tax could bring in enough revenue to substantially reduce the deficit over the next ten years. Alternatively, if the extra revenue is instead used to help lower income earners then the tax could be less regressive. If the additional money is used to reduce corporate income tax rates or other economic distortions, then the carbon tax could be used to mitigate some of its negative impact on GDP.

A discussion of this paper is provided by Don Fullerton.